Individual Housing Accounts

What this could mean for saving to stay in Hawai‘i

What is an IHA?

An IHA is a specialized savings account that is created as an incentive for Hawai‘i residents to become homeowners. It works by allowing people to put away savings from their income before taxes.

Terms to know:

Deduction: an amount of money that you subtract from your income and put into a savings account BEFORE taxes are taken out

Contribution: any amount of money that you deposit into a savings account

The difference? Deductions are SUBTRACTED from gross income, while contributions are DEPOSITED INTO an account.

What does this all mean?

How do I save?

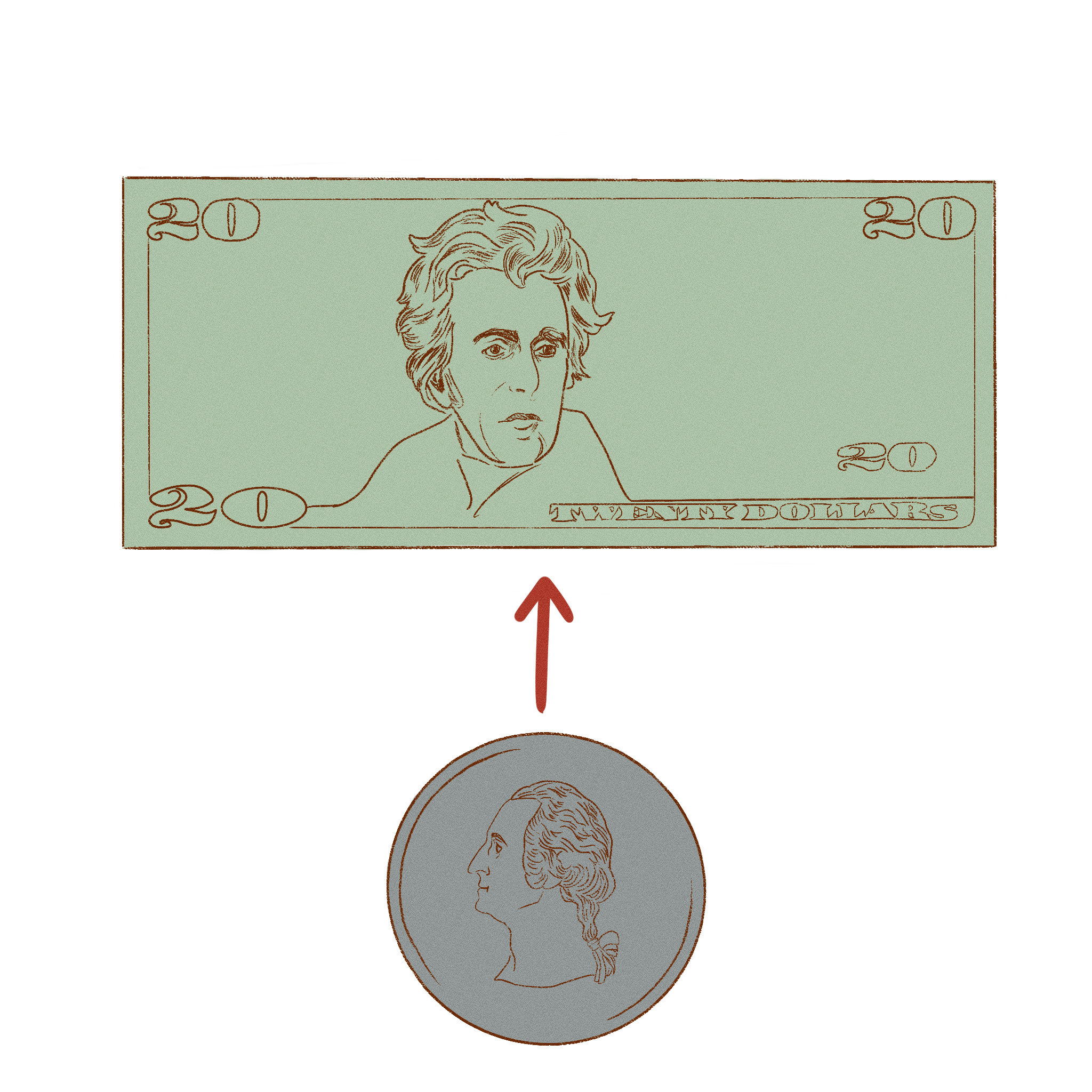

Without an IHA, someone earning a $100,000 salary who puts $20,000 away for a down payment would have that amount taxed at roughly 6.5%*, or $1,300. The new IHA rules make that $1,300 exempt from income taxes, meaning $1,300 additional savings a year for Kimo to keep—making it that much easier to save for that down payment.

If you’re chipping away at the goal of staying, the state is going to help by reducing your taxes and keeping in your piggy bank.

*this number is for example purposes; be sure to speak with your tax professional to tailor this to your specific scenario

The maximum annual deduction for contributions to an individual housing account is increased from $5,000 to $20,000 for individuals, and from $10,000 to $40,000 for married couples filing jointly. In other words, you can now put away $20,000 of your pre-tax income instead of just $5,000.

1. Increasing Maximum Annual Deductions

Why this matters: This means locals can more easily save for a down payment because funds put in an IHA are exempt from state income tax.

2. Increasing Maximum Account Levels

The total allowable deduction over all years is raised from $25,000 to $200,000, for both individuals and the sum of individual accounts held by married couples.

Why this matters: The old cap of $25,000 wasn’t enough to be impactful. The new limit of $200,000 matches the modern day cost of a home.

3. Focusing Eligibility on First-Time Homebuyers

The program is specifically designed for individuals, and married couples who have not owned a residential property within the last five years.

Why this matters: This strengthens housing affordability opportunities for young locals who may be starting out in their careers and looking to stay in Hawai‘i.

Do I qualify?

If you are a first-time homebuyer or haven’t owned a home in the past five years, you are eligible. The bill states that IHAs must be held at a qualified and insured financial institution in Hawai‘i, and funds are only tax-deductible if they are not withdrawn within 365 days and must only be used for the purchase of a home in Hawai‘i.

Who should you talk to?

Participating financial institutions will be coming soon!

Part of what we do at Housing Hawai‘i’s Future is push for solutions. One of our recent wins is the advancement of Senate Bill 2552 (SB2552), which relates to Individual Housing Accounts (IHAs) and how they can help local first-time buyers purchase a home in Hawai‘i.

According to the New York Times, Hawai‘i ranks lowest in the nation in homeownership among young adults under 35. This is largely due to the high cost of housing in Hawai‘i, with down payments on homes ranging in the tens to hundreds of thousands. SB2552 will refresh the IHA program that was established in 1982 to help first-time homebuyers save for their down payments. The greatest obstacle young people face is high costs, but this bill is designed to increase opportunities to put money into savings for first-time homebuyers.

Hawai‘i’s housing ecosystem has suffered from death by a thousand cuts; we hope IHA can be the first of many bandages to help fix the problem.

WHAT COMES NEXT

The policies with the strongest public support are the ones that treat housing as a cost-of-living solution - increasing home and rental availability, prioritizing high-need communities, and making it easier for working families to remain in Hawai'i.

If you want to be part of the conversation about Hawai'i's housing future, start here.